Let’s Talk About How to Calculate Your Net Worth | brokeGIRLrich

I think a really strong place to start with personal finance is to just assess where you are and creating a net worth statement can help you get there.

A cool thing about this step is you can sit down and do it right now and in an hour or two, you’ll probably have it done. Very few personal finance steps can just be achieved like that.

Also, it’s easy to get down or feel frustrated about our finances, but this first step should just be judgement free. Detach emotionally as best you can. You can pretend your Sherlock Holmes digging up clues for a case or a paleontologist assembling the bones of a prehistoric creature. You’re just gathering facts and information so you can make informed decisions going forward.

But what is this information we’re looking for. Simply, it’s all your assets and liabilities.

Assets are the money you have.

So you want to collect the balance you have on any:

- Checking Accounts

- Savings Accounts

- Retirement Accounts

- Investment Accounts

If you own a home and you have a reliable estimate on how much it’s worth, you can include that. If you don’t have a current reliable estimate, you can look at a few free home estimators and try to find a few recent selling prices for comparable homes in your area.

If you come up with a range you think your house would sell for, use the lower number. A tip I use is to always use the lower numbers or round down for assets and always use the higher numbers or round up for liabilities when you’re not sure of the exact number.

If you own a car, you can include the Kelly Blue Book value of the car. Again, when I do this I select that my car is in poor shape, which is the lowest rating it can give me, and use that number. I don’t actually think my car is in poor shape, but I feel confident I can likely get the number the Blue Book provides then if I needed to sell my car quickly.

That’s a key thing for any physical assets I include in my net worth statements. I think “if I needed to sell this on Craigslist tomorrow what would someone likely pay for it?”

In reality, with all the time to find the right buyer, these items would likely sell for more. Some people don’t include any physical assets in their net worth statements and that’s totally fine too.

Personally, because I have some inherited jewelry, some electronics I wouldn’t mind selling if I had to, and a few musical instruments I would part with in an emergency, I include them – all rounded down.

As a matter of fact, with the jewelry and electronics, I estimated what I could likely sell them for and cut it in half. The instruments are based on what a local music store would pay to buy them.

If you’ve never setup online accounts with the banks and brokerage and retirements accounts, now is the time to do that. On the plus side, you only have to do it once. On the negative side, I think the most tedious part of doing your net worth for the first time is hunting down all the account info to get those accounts open (this is the main reason I estimated this project could take up to two hours).

Finally, open up your wallet and count your cash on hand. Even if it’s only a few dollars, it’s still an asset.

I’d also recommend if you’re a college student or young adult doing this for the first time and you come from a family that has been able to provide you with some financial support, it’s worth mentioning to them that you’re trying to learn how to take charge of your finances and that you’ve been tracking your net worth. Sometimes parents or grandparents squirrel away a little for their kids and forget about it or are waiting till you seem “mature” enough to tell you about it.

Clearly, this isn’t a privilege everyone has, but when I mentioned this to my parents, my dad realized he had bought a life insurance policy for me as a kid that he paid like $2,000 for 20 years earlier. It was worth $9,000 something when I cashed it out and I used it to pay off a large chunk of debt. My mom remembered that my grandparents had been putting $50 of stock in an account for me on my birthdays for almost 25 years which had grown to a little over $3,000.

Again, I was totally lucky and $12,000 made a massive difference to me at 25 and they had literally just forgotten those things existed until I asked.

Once you’ve got all access to all your accounts sorted, you need to consider whether you want to track things yourself or sign up at a place that can track them for you.

Personally, I recommend tracking it yourself at first. I think the act of logging in and checking this once a month is a great habit to get into. But you know you best and if that’s going to be too much fuss, there are two great, free companies you can use to track your net worth:

They’re both free because they’re going to use all this data on you to advertise banking products and credit cards to you. So ignore that. Though also if you plan to open a new credit card or need a loan of some sort, their recommendations are often not bad.

With both of these companies, you sync your accounts and the net worth will automatically track.

I’ve had issues with both of them syncing some accounts though, so I still prefer using a trusty Excel sheet. I will say that my issues are just that I have to re-log in sometimes, so that may not bother you as much as it bothers me.

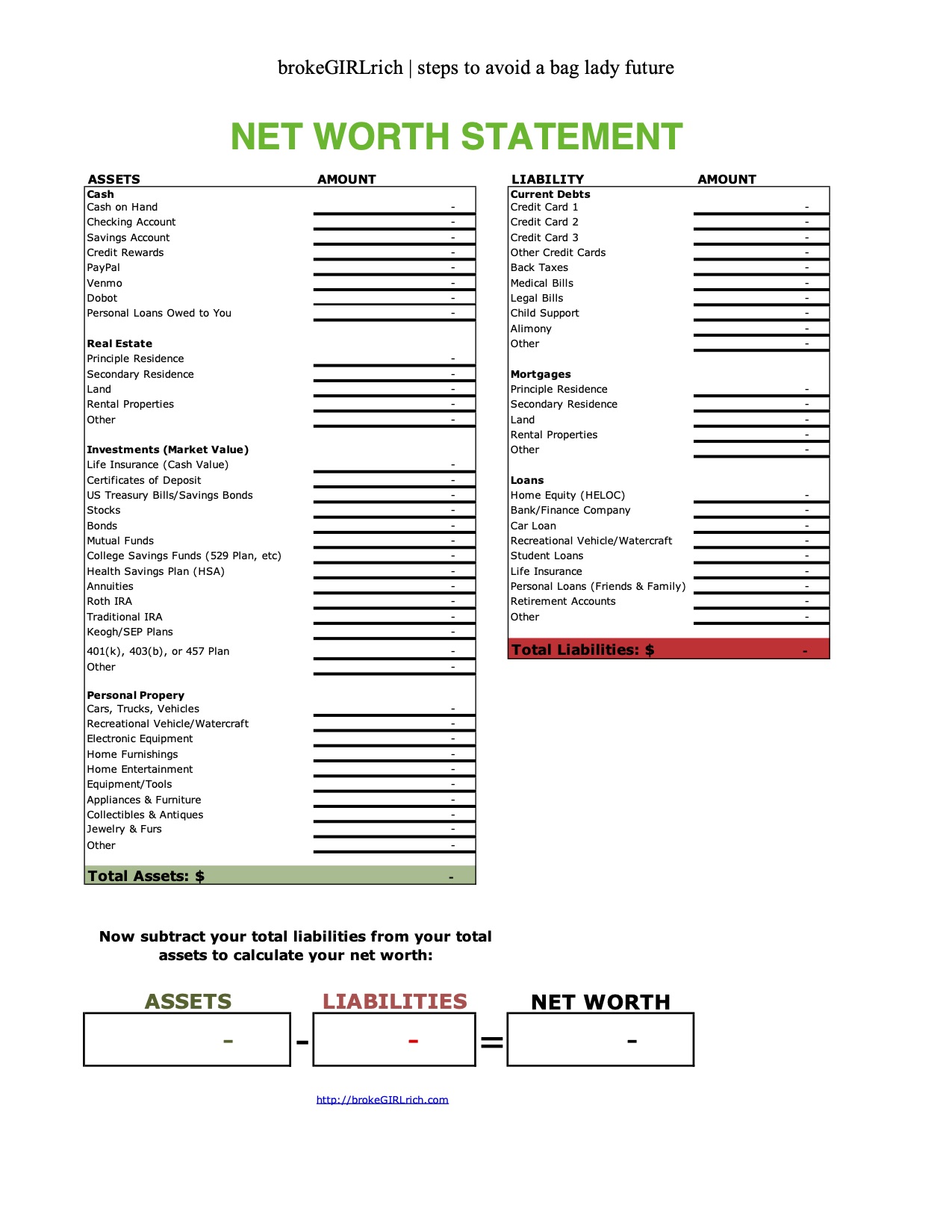

If you want to make your own Excel sheet, you can just list each asset and add them up to get your total assets.

Or, you can download the Excel sheet I use here:

Net Worth Statement Template

Or, you can download any of these free Net Worth Statement templates below, if you like how they look better:

- Money Under 30

- Budgets Are Sexy

- Family Balance Sheet

- The Millennial Money Woman

- Thirty Something Millionaire

Or, you can check out the plethora of templates on Etsy, which cost a few dollars, but if pretty paperwork is your thang, you might find it worth it. Seriously, I know some people are motivated by “making it pretty,” so if that’s you, it’s probably worth the $1-$5 for the pretty template.

You can also skip Excel altogether and track this on paper or in a bullet journal (which I don’t 100% understand what they are but they do seem like they would support tracking your net worth well).

Now we’ve done the fun side, which is figuring out how much money you have.

Liabilities is tracking what you owe.

So similar to assets, we’re just going to collect the information you need to log into each liability account you have. Those would be:

- Credit Cards

- Mortgage

- Loans

- Medical Bills

- Child Support

For each one of these, you want to figure out the current balance and add it to your net worth statement in the liabilities column.

Then you take your total assets – total liabilities = net worth.

At this moment, I’ll pause to give the most important disclaimer of the whole business, your net worth is not your worth as a human. It’s just a tool to use, a number to know so you can make a plan to get to the net worth you want in the long run.

If it’s deep, deep in the red, don’t feel alone. You’re not. There are lots of personal finance bloggers finding their way through life with a negative net worth.

If you’re breaking even or perhaps slightly in the green, there are a lot of personal finance bloggers trying to make smart money moves and learn more about personal finance to make sure it stays that way or gets even better.

- Get Rich Slowly

- Budgets Are Sexy

- Femme Frugality

- Bitches Get Riches

- and (cough, cough) brokeGIRLrich

If you’re killing it and looking for strategies to optimize your income even more or maybe retire early, you’re not alone either. There’s a whole group of personal finance bloggers speaking to that life as well.

I think one of the best things about reading personal finance blogs is learning you are not alone. There are people blogging about finance from every walk of life, which I find awfully reassuring.

So! You’ve got a number now. Congrats!

My next suggestion is that you revisit it every month. I honestly think the #1 personal finance tool I’ve used over the last almost 8 years is tracking. It kept me motivated when I was paying off debt and my bank accounts looked so sad but I could actually see progress on my net worth statement each month.

As things got a little easier, it kept me on track, because I could see if I was making bad choices before they became habits. It also helped show me the power of investing, even if it was only a little at first. That magic of investing doesn’t happen overnight but over time you definitely start to notice it’s benefits on your net worth.

Pingback: 100 Best Finance Blogs and Their Best Content (2021)