Budget 101: Mind Over Money

Most people seem to think that if they just had a little more money, they’d be so much happier, and to an extent this is true, but in a series of studies on the matter have shown that somewhere between $50,000-$161,000 is the optimum income (Kahneman, Frank, Wicker). That area is the money/happiness pinnacle. And if you really think about it, that can be a pretty achievable goal. It may take you a decade or two (maybe even three if you’re swamped in debt), but if you get a firm grasp on your money handling skills and learn a little about investing, this should be a goal we can all reach (I like to tell myself that anyway – I’m totally not there yet, but I am on my way there).

To start out down this path, we need to be aware of some of the tricks our brain likes to play on us. Such as when we’re out shopping and see the same item for two different prices, we often think the higher priced item is better quality, even if they’re exactly the same item.

Your personality type will also influence how you handle your money. People with high IQ’s tend to be very patient with money, but there’s no actual connection between high IQ’s and good financial planning skills (Grabmeier). There does seem to be a connection though between your personality type and self-control and people with greater self-control are likely to be much better with their money than those who do not – I’m looking at you, happy, sunny people. Evidence shows that the Pollyanna’s of the world are less likely to worry about their finances and more likely to want to give everything away to make the world a better place – and themselves flat broke. On the plus side, there is a fair amount of evidence that self-control can actually be learned. So take a few baby steps in that direction. Setting up a budget is a great start.

“One part of us is saying: ‘Buy it, you’ll feel real good!’ and another part is saying: ‘No, we need that money to pay the rent!’” – Jeremy Dean

People also fall into two categories – those who are prevention based and those who are promotion based (University of Chicago). Essentially the glass is half empty or half full. If it’s half empty, you’re probably prevention based and focus more on the negative effect of things to motivate yourself (looming credit card payments, going broke, living in a box under an overpass in retirement) and if you’re a glass is half full type, you probably are promotion based and use positive perks to motivate yourself (saving up for a trip you want to take, retiring early).

While shopping, you have to be on alert for even more crazy money pitfalls. Items that offer a 30-day money back guarantee are dangerous because people will buy things without thinking and figure they’ll return it if they don’t like it. Here’s a hint: You probably won’t. Most people do not return any of their 30-day money back guarantee items, even if they hate them. They just sit in a closet collecting dust. And because people often have “need to get my money’s worth” mentality, they’ll just a leave a $200 camera sitting in the closet instead of trying to resell it to recoup at least a portion of that loss (Carmon).

And watch out for your emotions too, as certain emotions trigger certain buying impulses. When you’re sad, you want to do anything to make a change, including impulsively buying items you usually wouldn’t. You’ll also sell things you already own for lower than you usually would. Disgust makes you less likely to buy anything and creates a strong desire to get rid of the things you already have. Anxiety makes you more likely to choose low-risk items (and investments).

The key thing to remember here is that changing your behavior and your attitudes toward money is going to be hard. It’s a mental equivalent of running a marathon because everything in your brain will scream against your newfound logic. If you’re used to retail therapy and crave that “buying stuff high,” it’s going to be as bad as quitting any other addiction. The trick to succeeding, like with most things in life, is to just do it. When it sucks, keep plugging along anyway. When you fail, get back up, dust yourself off and try again.

I’m sure if you’re reading my blog, you’ve checked out other personal finance blogs too, and they all say things like spend less than you make, put away cash in savings accounts, research your retirement account options. They range from broad statements that don’t really help anyone (well, maybe people who have never seen any of these topics before and are just feeling them out for the first time) to terrifically detailed how-to lists. The trick is to actually do them, mind over matter, until you start to succeed. And seeing your savings account numbers go up gives you the same, or an even better, high than a new pair of shoes.

Ramit Sethi wrote this great post on passive and active barriers to success and rounded it up with a great exercise I’m going to borrow.

1.) Write down five financial goals you’d like to achieve focusing on actions (ie: I want to put $20 in my savings account each week instead of I want to have $10,000 saved up for emergencies).

Why aren’t you doing it?

- I don’t have $20 a week to put in my saving account. Why?

- I like going out for drinks on Wednesday evening with co-workers. Why?

- Because it helps further my career. And I like vodka.

Solution: Limit nights out to once a week = No bar tab on Wednesday evenings = $20 into savings account

Clearly, it’s a little bit of an over simplification. And yes, you are losing out on some networking time. There is a good chance you can find those opportunities another way (what about organizing an intramural team or charity work?) and still save the $20. Maybe you’ve got that latte habit that all the personal finance blogs seem to think we all have or you buy too much nail polish and lip gloss (is that just me?)

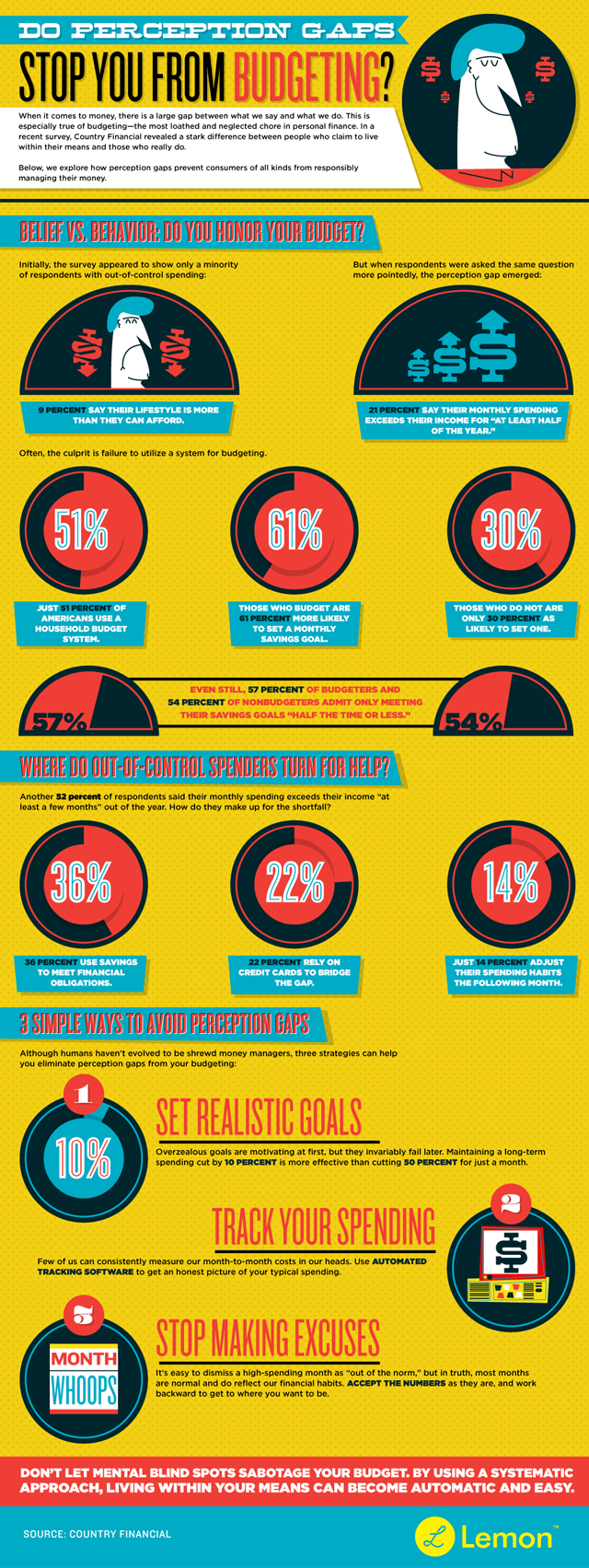

Do Perception Gaps Stop You From Budgeting? Infographic borrowed from Lemon via Business 2 Community

Sources:

Carmon, Z. and D. Ariely. “Focusing on the Forgone: How Value Can Appear so Different to Buyers and Sellers.” The Journal of Consumer Research 27.3 (2000): 360-370. Web. 17 Sep. 2013.

Frank, Robert. “Perfect Income for Happiness Around $161,000: Survey.” The Huffington Post. 2 Dec. 2012. Web. 17 Sep. 2013.

Grabmeier, Jeff. “You Don’t Have to be Smart to be Rich, Study Finds.” Research News. 24 April 2007. Web. 17 Sep. 2013.

Kahneman, Daniel and Angus Deaton. “High income improves evaluation of life but not emotional well-being.” PNAS 107.38 (2010): 16489-16493. Web. 17 Sep. 2013.

Sethi, Ramit. “The Psychology of Passive Barriers: Why Your Friends Don’t Save Money, Eat Healthier, or Clean Their Garages.” Get Rich Slowly. 17 Mar. 2009. Web. 17 Sep. 2013.

University of Chicago Press Journals. “Your Personality Type Influences How Much Self-control You Have.” ScienceDaily. 27 Jan. 2008. Web. 17 Sep. 2013.

Wicker, Alden. “The Price of Happiness: $50,000?” LearnVest. 24 April 2012. Web. 17 Sep. 2013.

People are so bad about sending in rebates and canceling free trials. It blows my mind that they’ll jump through hoops to save a buck here or two on other items, (like driving across town for gas), but then they’ll be so careless about others.

I know, it seems so strange to me too. I always put a reminder on my phone to pop up if I sign up for a free trial, so I can make sure to decide if I want to keep it or cancel it. I actually remember one particularly desperate point in college where I went through one of those mypoints.com type sites and signed up for every free trial that would get me points that I could turn into cash or gift cards. It was nearly a part time job canceling all those free trials!

By the way, I love your blog, especially your section on working in the arts. I’m a stage manager, so I totally sympathize with how ridiculous it is trying to make ends meet sometimes.

Pingback: Budget 101: Financial Goals | brokeGIRLrich